Zoopla's private equity strategy shift

/Zoopla recently announced that it has removed all non-property advertising from its listing pages. This is one of several significant strategy changes after its acquisition by private equity firm Silver Lake.

Why it matters: The benefit of being a private company is that Zoopla can be more aggressive, focus on longer-term opportunities, and be less sensitive to a stock price that focuses on short-term earnings growth. This move is an example of that strategy in action.

The advertising revenue dilemma

A number of real estate portals generate revenue from non-property advertising on their listing pages. Zoopla's move puts it in line with arch-rival Rightmove by banishing banner ads from listing pages.

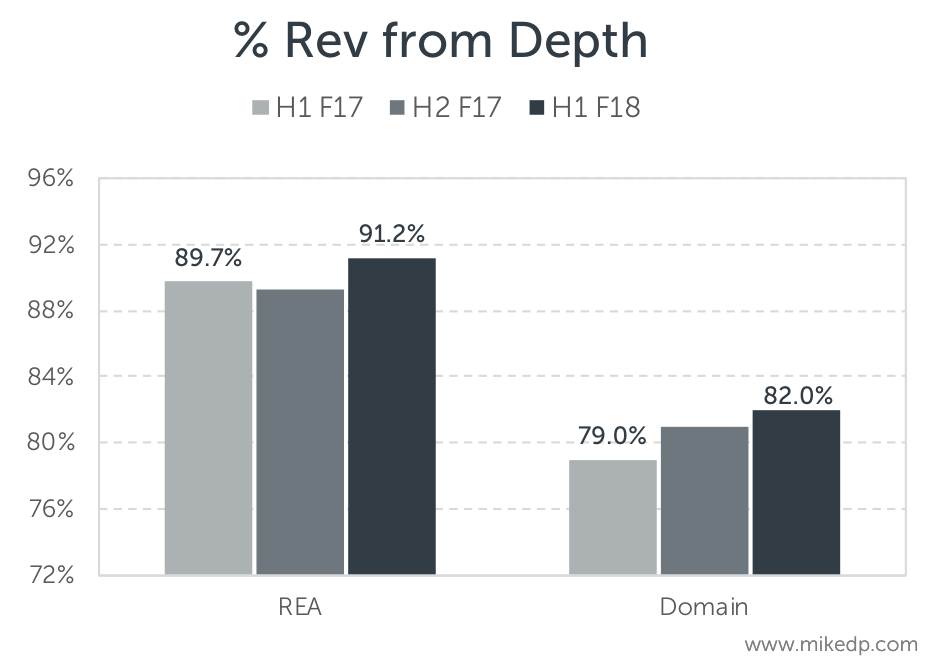

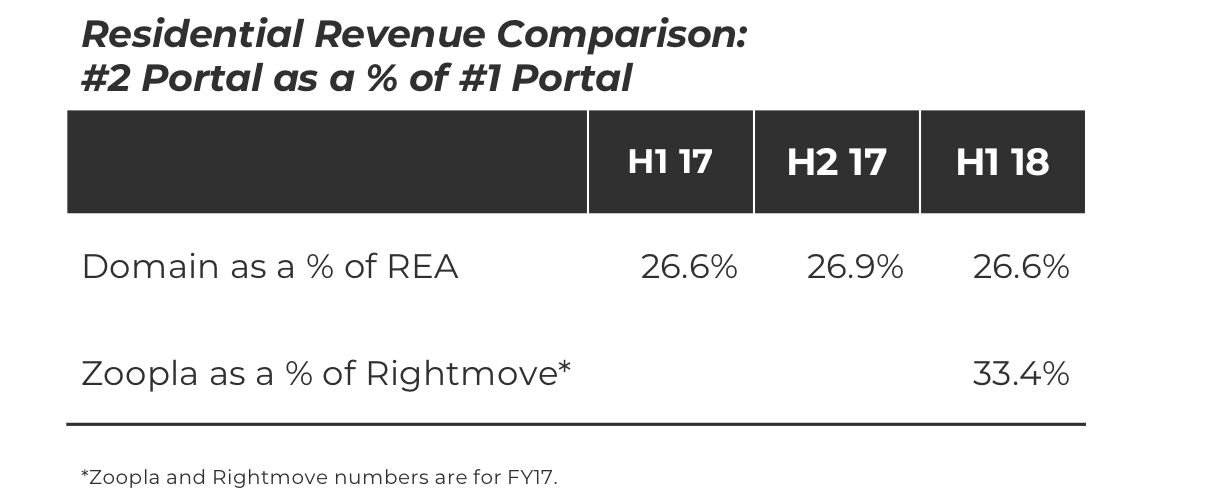

Note: REA Group and Domain do not have advertising on featured property listings, but do have non-property advertising on "normal" listings.

Banner advertising can be an important source of revenue for portals. However, it comes at the expense of the user experience. If a visitor clicks on a banner ad, their attention is diverted away from the property listing, reducing its effectiveness.

Often times user experience loses out to finances, especially for publicly listed companies under pressure to deliver revenue growth. And given that core revenue growth is slowing at a number of mature portals, the decision is even harder. But for a private company that's focused on the long-term opportunity, the decision is easy.

A shift in strategy

Aside from jettisoning nearly its entire management team, Zoopla has been up to quite a bit post-acquisition; there is the appearance of a significant change in strategy.

Zoopla's aggressive diversification strategy has been a leading factor making it unique in the world of real estate portals. It's been a world leader in acquiring adjacent businesses to dramatically grow revenues (for more on this, check out my 2018 Global Real Estate Portal Report).

The company's narrative has centered around a cross-sell strategy, where acquisitions are deeply integrated across Zoopla's network of web properties.

I've questioned the effectiveness of the cross-sell strategy, most recently in my Future of Real Estate Portals Report. The evidence didn't suggest a runaway success when it came to integration and cross-sell synergies.

Notably (and here's the big strategy shift), Zoopla's new managing director recently stated that, "Going forward, the former comparison and property businesses of ZPG will be managed largely separately, but we will continue to achieve synergies between the two wherever it is appropriate and relevant.”

To me, that sounds like a "back to basics" approach with a deep focus on the core product: tools for agents with a fantastic consumer experience. Cross-sell synergies and deep integration across the portfolio are taking a backseat.

Which is an interesting development for Scout24, which recently purchased financial comparison site Finanzcheck for $330 million, and Domain, which has been running the Zoopla diversification playbook for some time. Oops?

Strategic implications

Public companies that are focused on short-term revenue growth are at a distinct disadvantage to private companies backed by private equity. And private equity is getting more involved in the sector:

General Atlantic acquires a majority stake in Hemnet, December 2016.

Silver Lake acquires Zoopla for £2.2 billion, May 2018.

General Atlantic invests $120 million in Property Finder, November 2018.

Apax Partners offers $2.5 billion NZD for Trade Me, December 2018.

Rumors circulate that several private equity firms are looking at Germany's top portal, Scout24.

It's going to be difficult to compete with private equity-backed portals given their fundamental advantage: they can be more aggressive, focus on longer-term opportunities, and be less sensitive to a stock price that focuses on short-term earnings growth.