Opendoor's Buy-to-List Premium Falls Back to Earth

/

After reaching record levels earlier this year, Opendoor's buy-to-list premium (the difference between the purchase price and current listing price of a home) has fallen dramatically -- a reflection of a rapidly changing market.

Why it matters: The buy-to-list premium is the best leading indicator of iBuyer profitability -- and while it has dropped, Opendoor appears to be deftly riding a dynamic market.

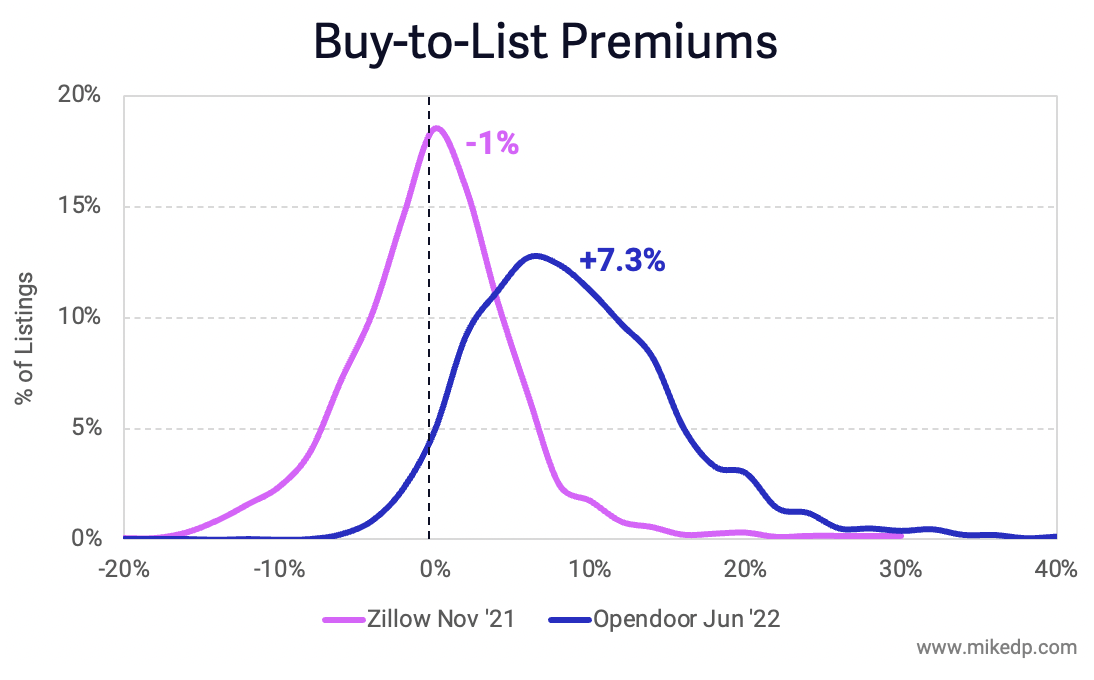

As of June 16th, Opendoor's median buy-to-list premium across 2,700 listings was 7.3 percent -- down from a record 17 percent in March.

Opendoor's home sale prices, as measured by the buy-to-sale premium, lags the market by a few months, and, for the time being, remains in very healthy territory.

In fact, Q2 is going to be another record quarter for Opendoor, with average buy-to-sale premiums over 10 percent according to YipitData.

A dropping buy-to-list premium is not the end of the world for Opendoor; it's not overpaying for houses or losing money on their resale.

Opendoor's buy-to-list distribution curve is significantly better than Zillow's was last year, when Zillow was, on average, losing money on each house resold.

The bottom line: The heady days of record home price appreciation -- the most significant driver of iBuyer profitability -- appear to be coming to a close (for now).

A buy-to-list premium of 7 percent is still healthy (and on par with the entirety of 2018 and 2019) -- but anything much lower, for longer, could present challenges.