Growth in new markets: An analysis of Opendoor, Knock, and OfferPad

/

Last December we conducted a wide-ranging analysis of Opendoor, the real estate startup that purchases homes directly from sellers. A look at of thousands of MLS records formed the basis of that piece, showing trends and extrapolating insights from the data.

At the time there were a number of unanswered questions we wanted to dig into: how much money does Opendoor make per transaction, how big could the model really get in the U.S., and does Opendoor have a sustainable competitive advantage against competitors?

Four months later I’m once again looking at the data, with these questions on my mind:

- What does Opendoor’s traction look like in its (relatively) new markets, Dallas and Las Vegas?

- Are there any notable changes in Opendoor’s fundamental business operations and metrics?

- Opendoor has two well-funded competitors in the market, Knock and OfferPad. How are they doing?

After looking at the data, there are three main observations:

- Dallas, Opendoor’s second market, is doing remarkably well. The transaction volumes there reached parity with Phoenix after only six months.

- Las Vegas, Opendoor’s third market, is off to a slow start. Key metrics suggest Opendoor is still finding its sweet spot in that market.

- Knock, Opendoor’s Atlanta-based competitor, is very early stage and has yet to ramp up in any significant fashion.

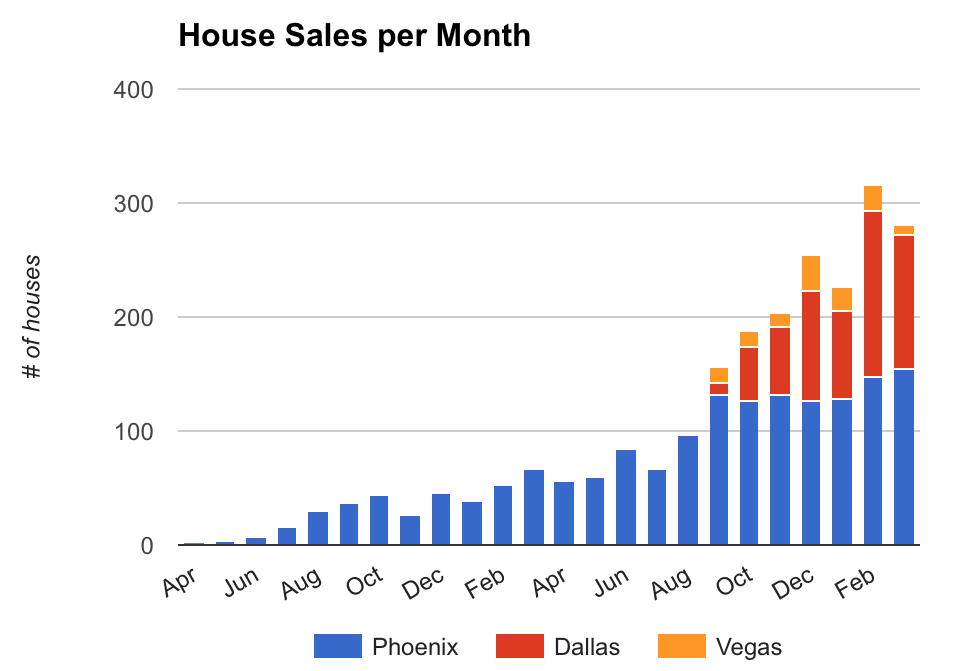

A snapshot of current volumes

Last time we looked at the data (at the end of November 2016), transaction volumes in Phoenix were going strong, Dallas was on a promising upswing, and Las Vegas was still small.

Since then, overall transaction volumes have surged from around 200 home sales per month to over 300 sales per month in February. In other words, in February, Opendoor was selling ten houses each day (including weekends) across all three markets. Not bad!

This growth appears to be driven by sustained volumes in Phoenix and very strong growth in Dallas -- putting that market on par with Phoenix after only six months.

Opendoor does Dallas

Let me be clear: I’m impressed with the growth in Dallas. When I’m evaluating new businesses and new business models (see my article, The Two Principles of Startup Success), I always look for business model validation (does this work in one market?) and then the ability to scale (can this be replicated in another market?).

Opendoor’s success in Dallas is a resounding answer to that question. Yes, the business can scale beyond one market. This is a noteworthy achievement for the firm.

Like Phoenix, the average selling price in Dallas is well-clustered. During the past three months, Opendoor’s median sale price in Phoenix was $210,000, compared to $212,000 in Dallas.

This suggests that, like Phoenix, Opendoor has found its sweet spot in the Dallas market. It deals with houses in a narrow and specified value range and (generally) does not deviate from that.

Opendoor credits its success to the team in Dallas and their focus on providing customers an experience they love. “We're seeing that customer love translate to growing word of mouth, and a growing business there,” said JD Ross, one of Opendoor’s co-founders.

What about Las Vegas?

I’m so glad you asked. Opendoor started listing and selling homes in Las Vegas at about the same time as in Dallas, last September. But growth has been slow ever since.

The sale price is not as well-clustered as in Dallas and Phoenix. There’s quite a spread of prices that Opendoor sells its homes for.

The median sale price in Las Vegas is also materially higher than Opendoor’s other markets, sitting at $322,000 (compared to $210,000 and $212,000 in Phoenix and Dallas). It’s not a factor of higher house prices in Las Vegas, either. According to Zillow, the median home price in Las Vegas is $209,000 and the median listing price is $247,000 -- which is on par with Phoenix and Dallas.

In Phoenix and Dallas, Opendoor is selling homes for roughly the market’s median home price. But in Las Vegas, it’s considerably higher.

Opendoor has been selling homes for six months in Las Vegas; perhaps its median sale price started high but has been falling to normal levels over time? Nope.

There’s a noticeable oddity in the Las Vegas market, with slow growth, a less-clustered sale price, and a sale price that’s higher than normal. Why?

It’s because Opendoor’s approach to the Las Vegas market is different. “In Vegas we've been focused on partnerships, and haven't pushed to expand to the broader market there yet,” says JD.

This is a different approach than Opendoor has taken in its other markets, with correspondingly different results.

Opendoor has partnered with Lennar (a new home builder) to offer the Lennar Trade Up program for Las Vegas homeowners. It’s a way for homeowners to “trade in” their existing homes to Opendoor as part of a package to buy a new home from Lennar.

This is a different approach than Opendoor has taken in its other markets, with correspondingly different results. My guess is that it’s a lower-cost option for the firm that effectively outsources lead generation to a partner while allowing Opendoor to focus efforts elsewhere. In other words, it’s a test, which is exactly what a you’d expect from a young, growing company.

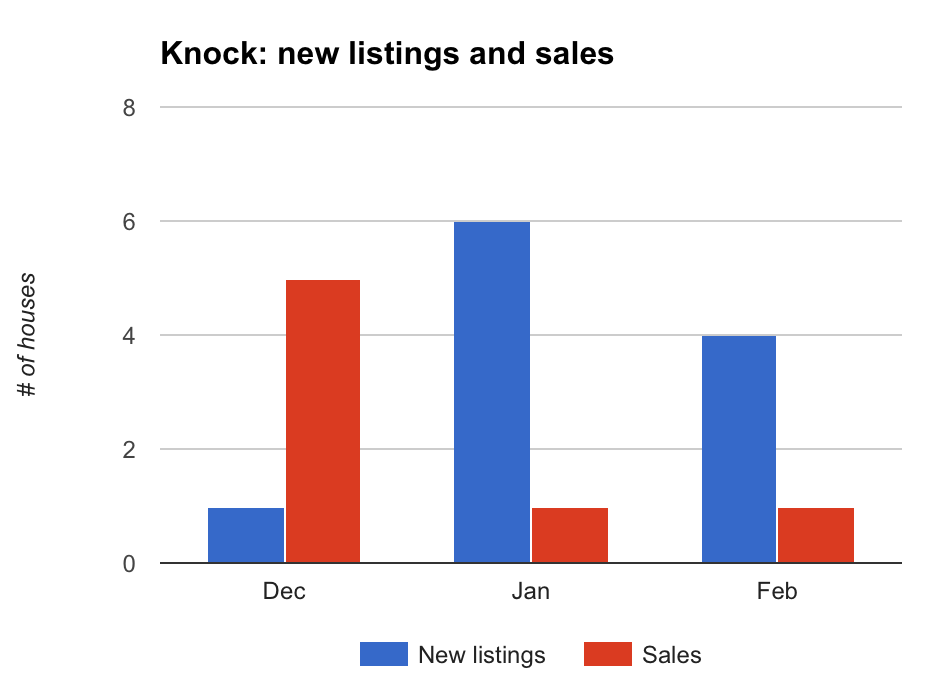

Knock, Knock

Since the last analysis, two well-funded competitors have entered the U.S. market: Atlanta-based Knock and Phoenix-based OfferPad. Both announced that they raised over $30 million each in January of this year.

Knock is live in Atlanta and currently trading with tiny volumes; we’re talking about one home sold each of the past two months. It also has a very small number of new listings each month, anywhere between one and six over the past four months.

Knock either does not have the price discipline we’ve seen work so successfully for Opendoor, or is not yet enforcing it.

The median sale price for Knock’s ten listings that sold is $290,000. But underneath that, if we look across all listing prices, you can see they’re not clustered at all. The home values are all over the show, meaning Knock either does not have the price discipline we’ve seen work so successfully for Opendoor, or is not yet enforcing it.

There are several key takeaways in looking at Knock:

- This is a difficult business to be in. Raising money doesn’t give you market share. It takes time, skill, and good operations to build scale.

- Knock is super early stage. Its transaction volumes suggest it is still tinkering with its core operations and proving it can make the model work before attempting to scale up.

- Price discipline is important. It may be tempting to deal with higher-value homes where the fees are correspondingly higher, but Opendoor has shown us where the sweet spot for this model really is.

OfferPad, on the other hand, is a more mature business with better traction -- at least in the Phoenix market. With the help of friends at ATTOM Data Solutions, a real estate data company that aggregates data directly from property records (as opposed to my usual MLS sources), I was able to gather a snapshot of relative traction for both businesses in Phoenix.

It's worth a deeper dive into OfferPad, its model, and relative merits. But that will have to wait until another time.

A look at Opendoor’s operations: anything interesting?

To wrap everything up I took a quick look at Opendoor’s core business metrics to see how things are tracking.

To begin with, the much-talked-about home value appreciation has stayed the same with a median average of 5.4% (looking at 43 recent sales). That’s the difference between what Opendoor buys a home for and eventually sells it for -- about $11,000.

And listen: That’s the difference between the buy and sell price. Opendoor takes on a number of costs associated with sprucing up, holding, and selling a house. So don’t confuse that number with profit; it’s not.

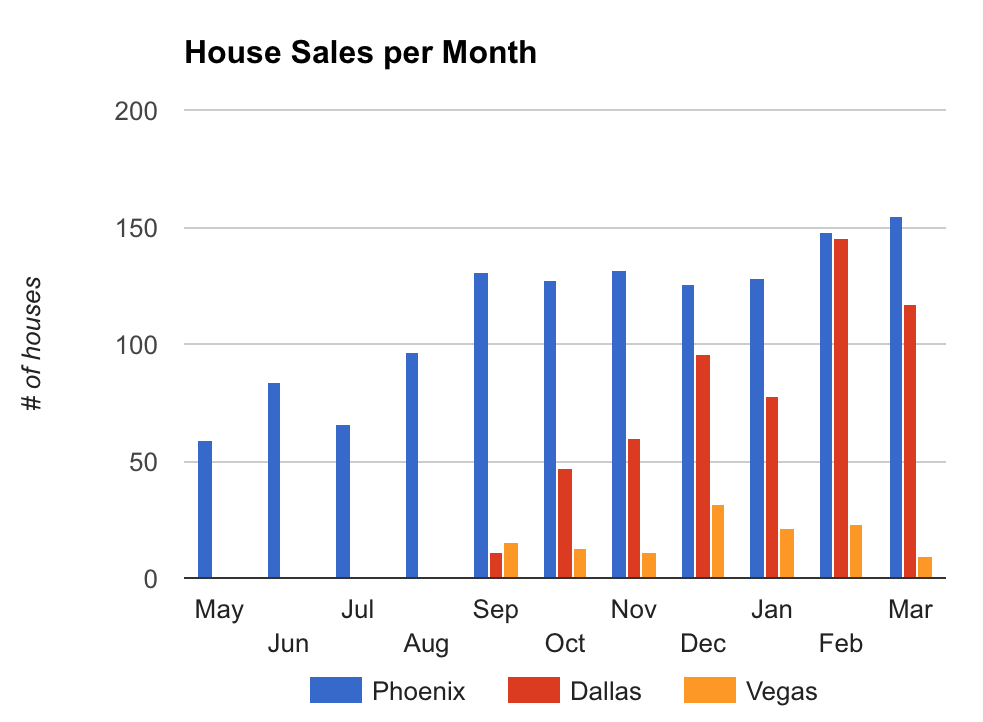

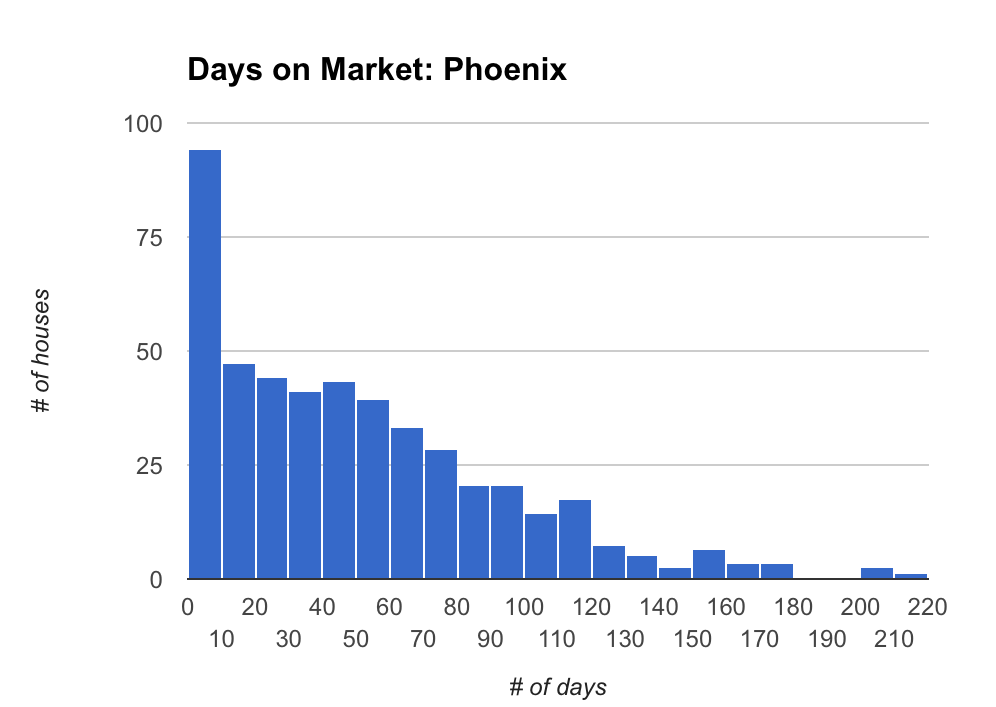

If you prefer small dots to blue bars, below is another way to visualise the same data.

The average days on market in Phoenix has seen a slight improvement, moving down to a median average of 41 days from 47 days in the last analysis. That’s a 12% improvement, which if I were running the business I would have as a key metric. It’s a small improvement -- but when time is money -- a welcome one!

Opendoor also has a new logo.

It will be interesting to watch Opendoor’s progress from here. With Phoenix and Dallas firing well, will it expand to a handful of new markets, or is Las Vegas the next area of focus? When it enters new markets, will it follow the partnership model? And will Opendoor launch in Atlanta before Knock puts the foot down on the accelerator?

Are you researching iBuyers like Opendoor and on the hunt for data? Do you work at a consulting or venture capital firm? Check out the iBuyer Analysis Pack.