Is Realtor.com in it to win it?

/On March 7th, this report on Realtor.com owner News Corp piqued my interest. Chief Executive Robert Thomson, referring to Realtor.com, said, "Obviously we’re in a competition, long term, to be number one..."

He went on to say, “...I think it’s fair to say that we turned what was the number three company into a very strong number 2 and, depending on the quarter, depending on the metric, in some quarters the fastest growing."

Here's the thing: I don't think Realtor.com is really competing to be number one.

Growth metrics

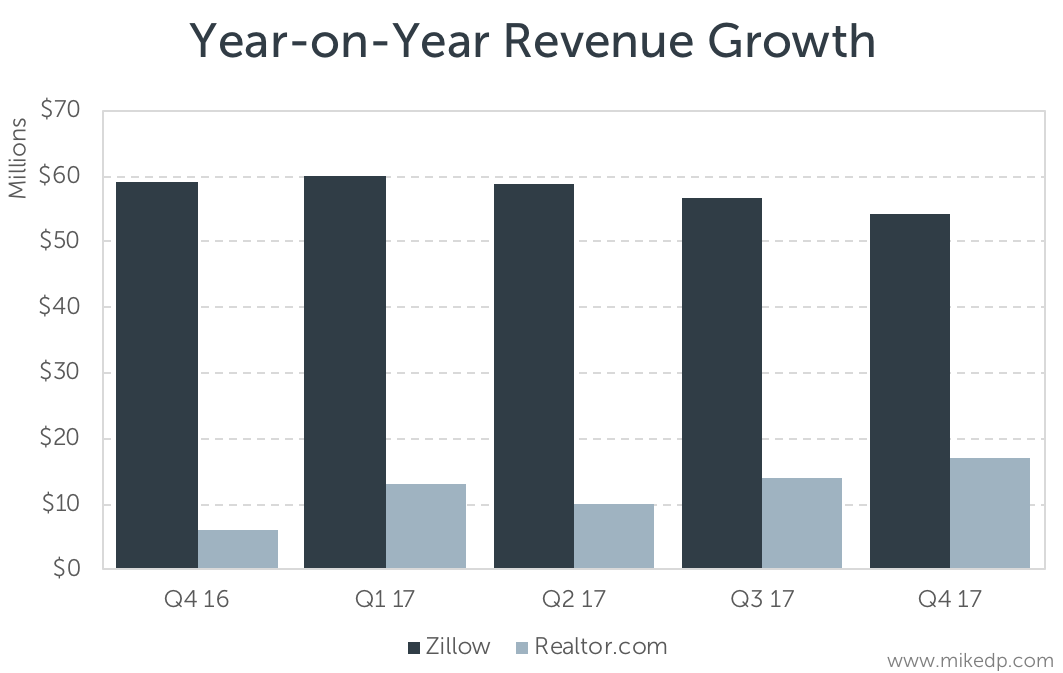

If we look at the most important metrics, I don't see evidence that Reator.com is the "fastest growing" in any category. These self-reported traffic metrics are essentially static: Zillow has around 3x the traffic of Realtor.com.

Zillow is growing its revenue (from a larger base) considerably faster than Realtor.com.

On a quarterly basis, Zillow blows away Realtor.com in terms of year-on-year revenue growth (again, from a much higher base).

The last chart does show an interesting trend, which is slowing revenue growth at Zillow compared to rising growth at Realtor.com. But in absolute terms, during the last quarter Zillow increased its revenue by $54 million while Realtor.com increased by $17 million -- a big difference!

There's still a lot of distance between the two, but it's true that Realtor.com is trending upwards while Zillow's revenue growth is slowing.

I'm not sure I'd agree that Realtor.com is the "fastest growing" in any meaningful metric, but the last three quarters show the start of a promising trend for the business.

Is Zillow concerned?

If Zillow were genuinely concerned with Realtor.com's growing momentum, I'd expect its sales and marketing expense to increase. If Realtor.com's market share were growing, Zillow would be spending more advertising money in response.

Aside from a slight bump a few quarters ago, Zillow's sales and marketing expense as a percentage of revenue is relatively flat and trending downwards.

Serious competition for top spot?

You can't argue with the fact that Realtor.com would like to be the #1 portal in the U.S. market. But are they really in a serious competition to be #1?

News Corp has been a major investor in REA Group, the leading portal in Australia, for almost two decades. More than most, it understands the power of network effects and how expensive and futile it can be to unseat a #1 player.

So is News Corp realistically expecting to overtake Zillow in the U.S.? I doubt it. I believe it's happy to run slipstream to Zillow and operate a strong, profitable business in its own right, but remain the #2 player. Attempting to overtake Zillow would be incredibly expensive and uncertain, and the resulting marketing war would drain all profits from both companies.

News Corp would never admit this strategy (who would admit they're happy to be the runner-up?). Being the underdog and striving to overtake the market leader is a great story and good for morale, but it will probably remain just that: a story.