Inside Compass — Part 4: Sustainability

/Part One of this series took a detailed look at Compass’ growth strategies, while Part Two examined if Compass is a tech company, or a traditional brokerage, and Part Three looked at Compass’ $4.4 billion valuation compared to its industry peers.

Part Four of this series looks at sustainability. Can Compass keep up its aggressive — and expensive — acquisition strategy? Will agents, without whom Compass wouldn’t generate any revenue, remain happy and stay under the Compass banner? And perhaps most importantly, can the company generate a profit?

The search for profitability

Compass is not profitable. Given its massive expenditures — both to support its brokerage acquisitions and to support its growing employee base — there’s simply no way it can be making money. Nor should it be (yet).

Compass is a growth stage business, investing today for a more powerful and profitable tomorrow. The question for all growth-stage businesses is whether they can ever achieve profitability. A number of other real estate industry behemoths are also unprofitable on a GAAP basis: Zillow, Redfin, Opendoor, eXp Realty, and Purplebricks.

Compass, like all private companies, does not need to share its financials. But with the data is does make public, in addition to benchmarks against public company peers and a few educated assumptions, we can paint a rough picture of its financials. To refine my thinking for this analysis I’ve spoken to dozens of industry executives and insiders, including leaders of top brokerages, independent analysts, and current and former Compass employees and agents.

Revenue and gross margins

Compass ended 2018 with around $900 million in revenue (source: Robert Reffkin’s letter on Inman). Like its real estate brokerage peers, eXp Realty and Realogy, that number includes the full real estate commission, only a fraction of which Compass retains. A large percentage of that number is paid directly to agents (70%–90%), with a smaller percentage retained by Compass as its gross profit. This is the commission split.

According to REAL Trends, which has been tracking the residential brokerage industry for decades, the average retained revenue (gross profit) of brokerages was 14.9 percent in 2018. The sample size is 200–300 of the largest U.S. brokerages.

High producing agents typically command more favorable commission splits as high as 90/10 — with only 10 percent retained by the brokerage. There is anecdotal evidence (including a number of agents I’ve spoken to, agents that Compass attempted to recruit, and brokers that have lost agents to Compass) that in some cases Compass offers 100 percent commission splits as a recruiting incentive, either for a certain amount of time or a fixed number of deals.

This is confirmed by the Wall Street Journal, which reports, “The firm has lured top talent with some of the most generous commission splits in the business: Some agents received all the sales commission, with nothing going to Compass, on as many as eight of their first deals, according to offer letters.”

eXp Realty, another self-proclaimed tech-enabled brokerage with revenues of $500 million in 2018, has 8 percent gross margins. eXp Realty also offers favorable commission splits with a cap on fees, and is the best benchmark available for Compass. It’s likely that Compass’ gross margin is in the 10–12 percent range, and for this analysis I’ve assumed 12 percent, resulting in $108 million of gross profit in 2018.

Operating expenses

Estimating Compass’ operating expenses is more complicated. I’ve used three different methodologies in order to provide a range of data points:

Operating expenses as a percentage of revenue

Operating expenses as a percentage of gross profit

Build-up approach

(Readers are encouraged to download the companion Excel file and plug in their own assumptions. It’s a choose your own profitability adventure!)

Compass has four publicly listed peers with similar business models: Realogy, eXp Realty, Redfin, and Purplebricks. Each company reports and breaks out operating expenses into various categories, including technology, marketing, and general and administrative. It’s straightforward to calculate each company’s operating expenses as a percentage of overall revenue, and as a percentage of gross profit.

On average, the four industry peers’ operating expenses are 32 percent of revenue and 113 percent of gross profit (Redfin and eXp Realty are unprofitable). Applying those same averages to Compass suggests operating expenses of between $122 million and $288 million in 2018.

The build-up approach for operating expenses focuses on known data: employee headcount and office expenses. Based on the same source of information, here’s what is known:

Compass had 238 offices at the end of 2018

Compass had around 1,500 employees at the end of 2018

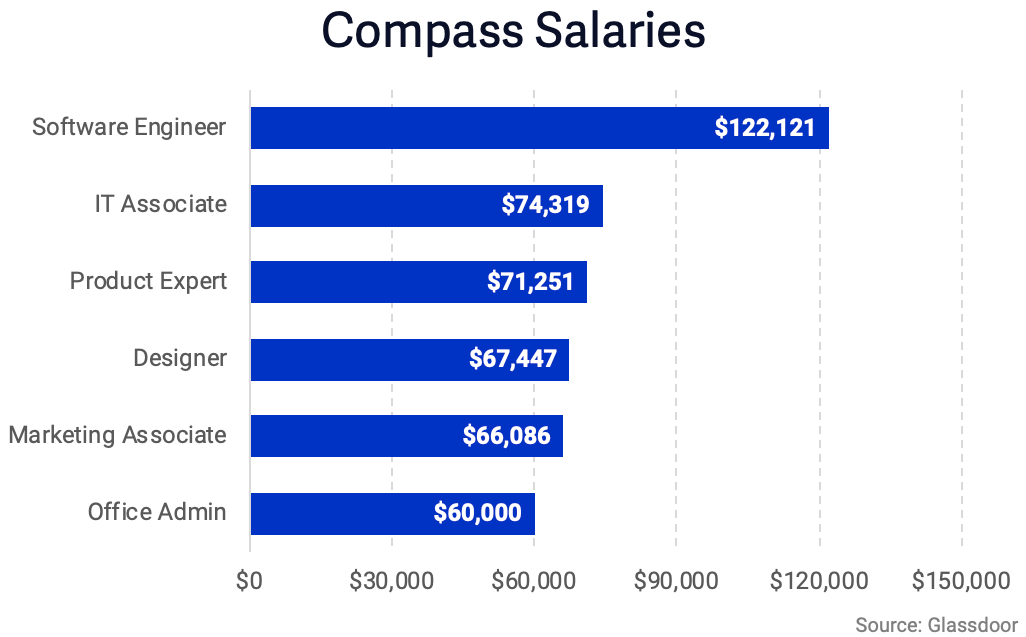

Compass operates in expensive metro markets like New York City, San Francisco, and Seattle, so employee costs are on the high end of the spectrum. According to a review of 250 employees on Glassdoor, the average salary for a Compass employee is $72,000 per year (ranging from $60k for an office administrator to $120k for a software engineer).

That figure doesn’t include benefits; according to the U.S. Department of Labor, on average, employee benefit costs account for around 30 percent of total employee costs. That would put total employee costs at $100,000 per head (salary plus benefits), resulting in an annual staff cost of $150 million for Compass’ 1,500 employees.

For office space, several industry insiders and CEOs of top brokerages claim that 75–100 square feet of office space per agent is a reasonable benchmark. Cushman & Wakefield reports that the national average, across all industries, is 194 square feet per employee. I’ve assumed an average of 83 square feet per agent, or 3,500 square feet for each of Compass’ 238 offices.

Compass pays from the mid-$60s to mid-$70s to $80 per square foot for some of its NYC offices, and $54 per square foot for a San Diego office. I’ve assumed an all-up expense of $60 per square foot, resulting in a total annual rent cost of $50 million.

Employee and office space expense alone totals $200 million. This figure doesn’t include a number of other one-time and ongoing expenses, such as sales and marketing and office fit-outs, which would push that number even higher.

This figure is Compass’ expense run-rate, based on figures from the end of 2018, a year which Compass grew its employee count and office space incredibly fast. Taking a mid-point average (150 offices and 1,000 employees) yields an employee plus office cost expense of $132 million for 2018.

(Based on this June 12, 2019 update from Compass, there are currently 2,500 employees. Assuming 248 offices, the current employee plus office expense run-rate is $300 million per year (not including other operating expenses), up from the $200 million mentioned above.)

Based on rough industry benchmarks, Compass’ operating expenses could range anywhere between $122 million and $288 million in 2018 (quite a range). But the build-up methodology suggests it was closer to $150—$200 million.

Operating expenses of between $150 million and $200 million in 2018 are nearly double Compass’ gross profit. In other words, Compass would be spending between $1.50 and $2 for every $1 in gross profit — not including its brokerage acquisition costs (which I previously estimated to be between $220 and $240 million, paid in a combination of cash and stock).

Profitability Catch 22

In its march towards long-term, sustainable profitability, Compass faces a dilemma. Like other brokerages, its gross profit is directly tied to the commission splits it offers agents. Profitability is a Catch 22: reducing commission splits for agents increases gross profit for Compass, but makes the company a less appealing home for agents.

Compass must look elsewhere for new sources of revenue — but it’s unclear where.

Compass’ chief operating officer told the Wall Street Journal, “We’re not yet at a stage where I have a very clear monetization strategy because we haven’t really talked about it.” Its CEO said the company plans to make money through ancillary services like title, mortgage and insurance services, but it’s not clear how. “Short term profitability is something that many of the more modern companies are not as focused on,” he added.

To grow revenues, Compass needs more agents closing more deals, and — unless something radically changes — those agents will require more, not less, support staff and office space. To reduce expenses, Compass would need to trim its full-time headcount or slow the hiring of support staff, or consolidate and close a number of its offices — both of which run the risk of making Compass a less attractive brokerage partner for agents.

The options available to Compass — optimizing the commission split and generating revenue by selling mortgages — are the same available to other real estate brokerages, and in fact, what they have been doing for years. Going down that path is an old game plan, which is why it’s unlikely to be Compass’ destination. Investors didn’t pump over $1 billion of venture capital into Compass to build “just another brokerage.”

Endgame

This analysis presents a thorough look at what Compass is doing; the alluring, unanswered question is why.

The company is deploying an aggressive acquisition strategy to acquire agents and brokers to build market share, is positioning itself as a tech company, and sports a sky-high valuation based on its growth rate and future plans — but what are its future plans? How does it plan to turn the existing, unprofitable brokerage business into a mammoth of the real estate industry? This is the topic of the next and final installment of this analysis: Endgame.

{kind=link}