The Real Estate Portal + Mortgage Conundrum

/

The largest global real estate portals are attempting to diversify and expand their revenue streams by offering mortgage -- with mixed success.

Zillow, Redfin, and Australia's REA Group have all made major forays into mortgage with large acquisitions.

Despite being technology companies, revenue growth is closely tied to employee count, and profitability (in the U.S.) remains elusive.

Dig deeper: Redfin's mortgage revenues jumped after its recent acquisition of Bay Equity for $138 million, but the overall business remains unprofitable.

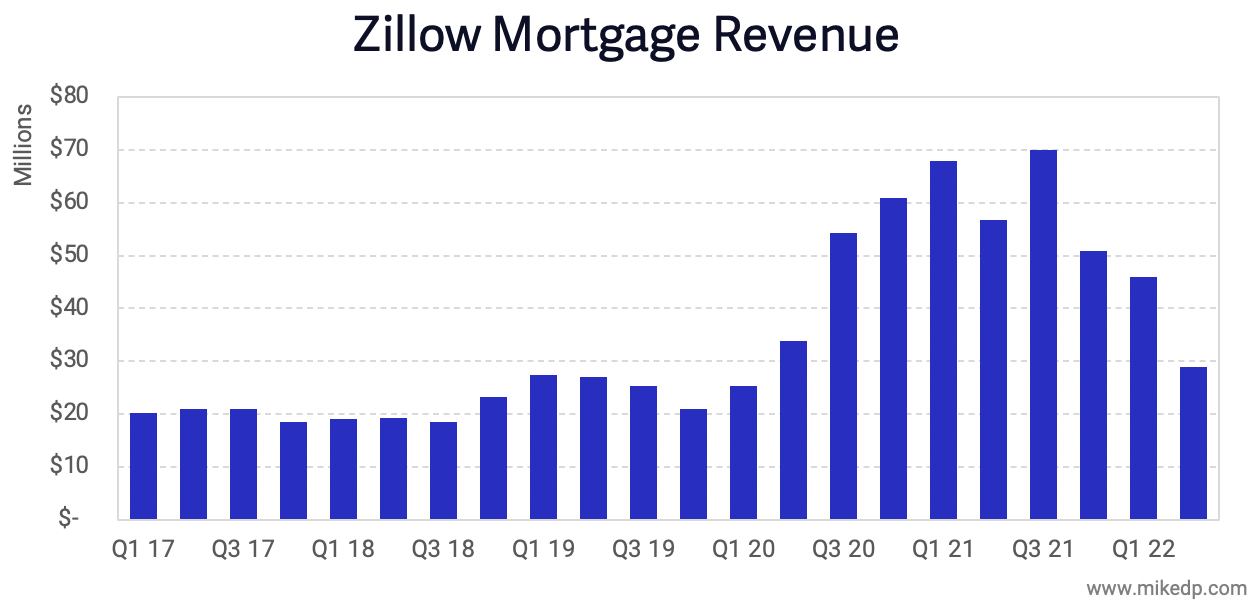

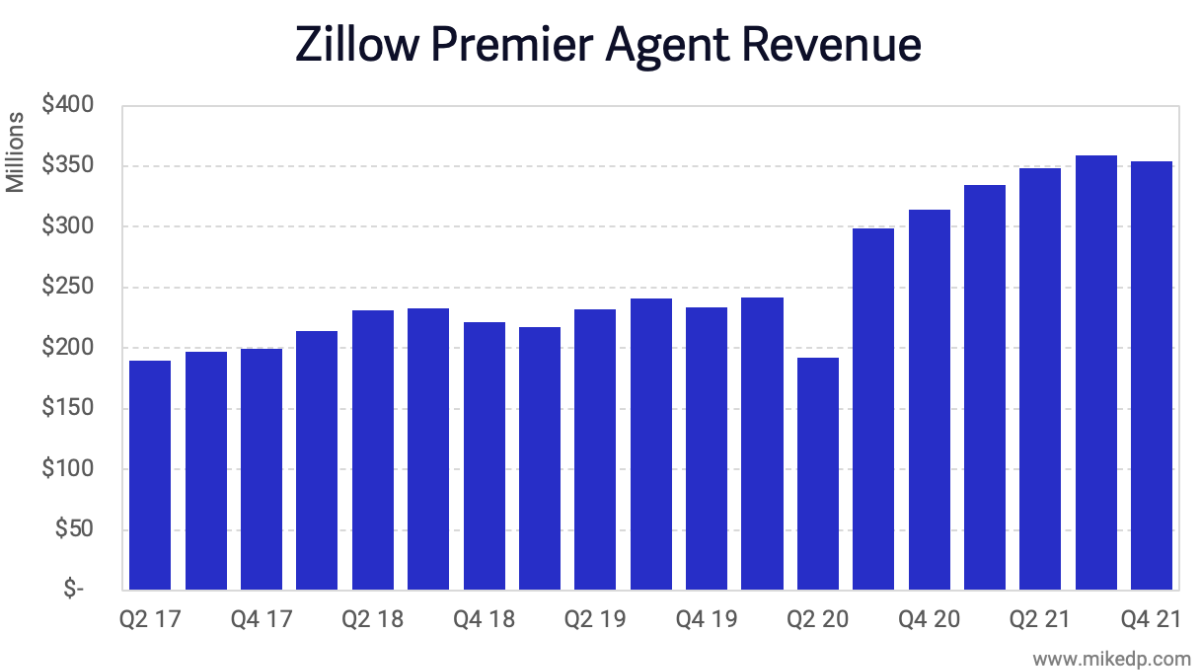

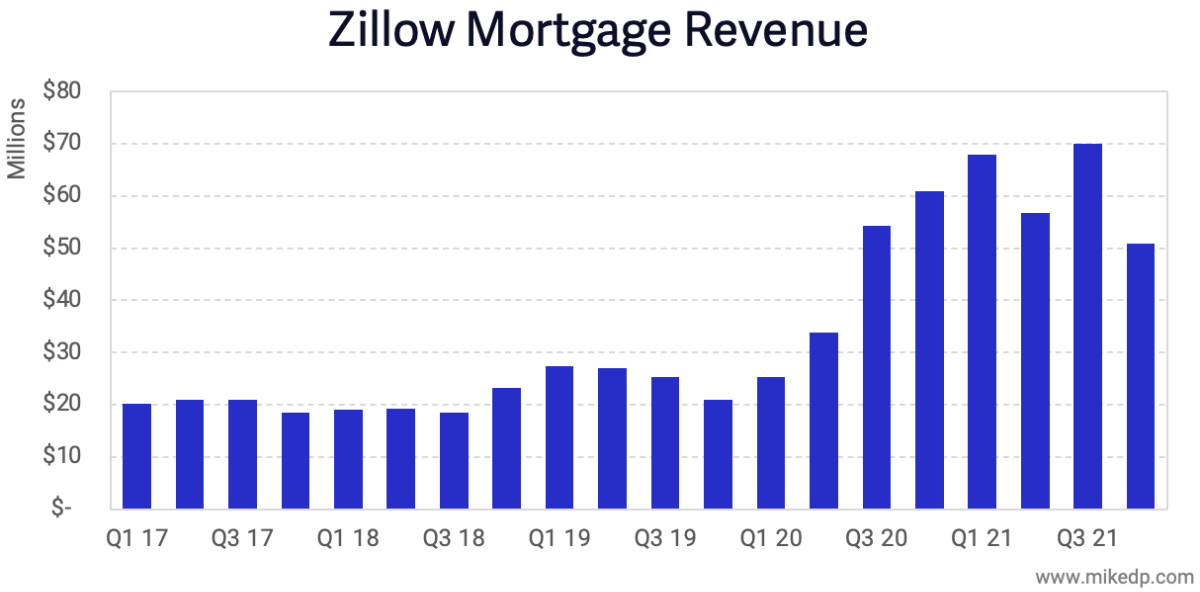

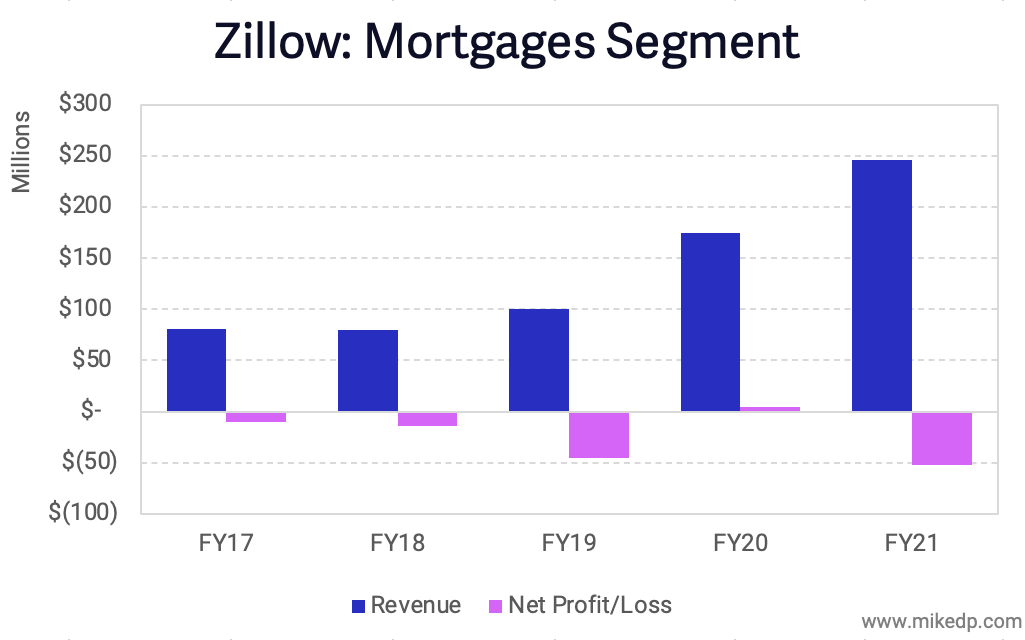

Zillow's mortgage business has been unprofitable for over five years, recently spending $1.85 for every $1 in mortgage revenue.

It even lost money in 2021, when 96 percent of mortgage firms were profitable.

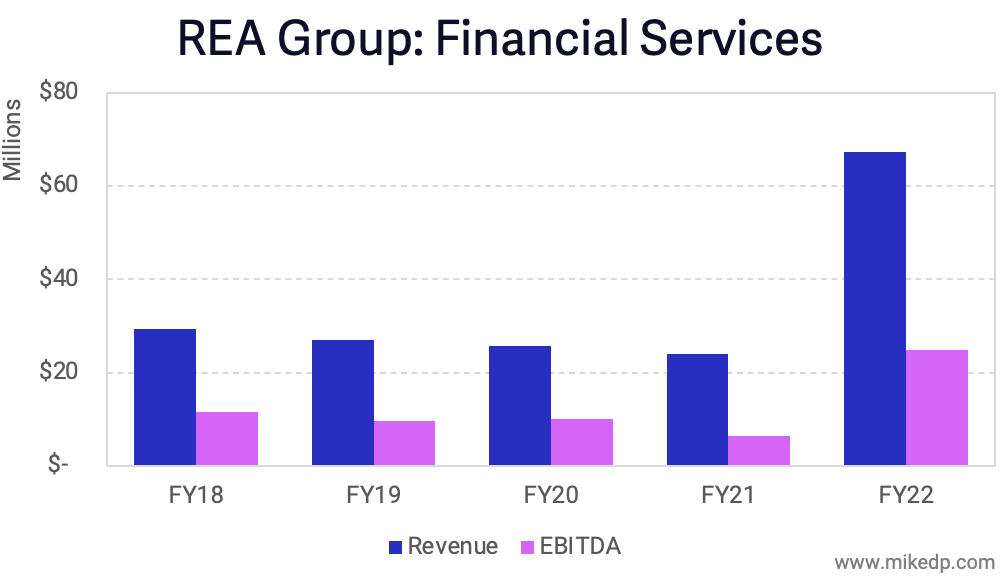

Australia's leading portal, REA Group, has managed to grow a profitable financial services business by acquiring two large mortgage broking businesses.

Financial services now accounts for six percent of REA Group's total revenue.

Behind the numbers: Mortgage growth is very much tied to people -- mortgage brokers and mortgage loan originators (MLOs).

REA has acquired legacy mortgage businesses with hundreds of brokers -- the company currently employs more than 1,000 brokers.

Redfin's mortgage originations jumped in Q2 2022 after its acquisition of Bay Equity and its 485 MLOs.

Mortgage business growth is tightly correlated to an increase in mortgage advisors (brokers and MLOs).

Redfin's mortgage originations are up 10x while MLO count is up 12x after acquiring Bay Equity.

REA's financial services revenue is up 2.8x while its number of mortgage brokers is up 2.7x after acquiring Mortgage Choice.

Broader context: The number of MLOs is an important bellwether for the ability of other real estate tech disruptors to grow in the mortgage space.

Some companies have shed MLOs through recent layoffs (Reali, Tomo, Homie, Knock, and Flyhomes), while others have grown organically and through acquisition (Orchard and Homeward).

The bottom line: Billions of dollars are being invested to disrupt the mortgage process -- which is the path to profitability for many real estate tech companies.

Instead of leading to greater profits, mortgage has turned into a money pit for the big U.S. real estate portals.

And at the end of the day, the evidence is clear: it's the number of brokers and MLOs that drives meaningful business growth.